The Half Sandwich Generation: 'I’m child-free with aging parents'

+ The Dirty Dozen & The Clean 15 of fruits and veggies

The Dirty Dozen

What if our fruits and veggies aren’t all they’re cracked up to be?

We all know we need to eat more plants to live longer, but what if pesticides cancel out the health benefits?

A study in the International Journal of Hygiene and Environmental Health tracked nearly 1,900 adults and found that people who ate more high-pesticide-contaminated produce had measurably higher pesticide biomarkers in their bodies — particularly for organophosphate, pyrethroid, and neonicotinoid insecticides.

What does this mean for your health?

SuperAge says we don’t know with certainty at dietary exposure levels. “The strongest evidence for harm comes from occupational exposure, not your salad. But associations at lower levels exist and are worth taking seriously.”

The down and dirty: This is absolutely not a reason to eat fewer vegetables. But it’s good information to keep in mind.

The “dirtiest” produce

Pesticide residues were found on 96% of these items, with 203 different pesticides detected across the 12 produce types. Long story short: Buy organic when possible.

Spinach

Strawberries

Kale, collard and mustard greens

Grapes

Peaches

Cherries

Nectarines

Pears

Apples

Blackberries

Blueberries

Potatoes

Honorable mentions: SuperAge reports that bell and hot peppers and green beans ranked just outside the dozen but topped the list on toxicity of detected pesticides.

The Clean 15

Nearly 60% of samples from the following list had no detectable pesticide residues, reports SuperAge. Don’t worry so much about buying organic, and save your budget on:

Pineapple

Sweet corn

Avocados

Papaya

Onions

Frozen sweet peas

Asparagus

Cabbage

Watermelon

Cauliflower

Bananas

Mangoes

Carrots

Mushrooms

Kiwi

4 tips to reduce pesticide exposure

Single out your top 5 '“dirtiest”. Which Dirty Dozen items do you eat most frequently? For example, if you eat grapes every day, they’re a higher priority swap than, say, summertime peaches.

Wash everything under running water. A 2022 study found that washing leafy vegetables under running water reduced pesticides by an average of 77% — beating out detergent washes.

Clean apples with baking soda. A dilute solution (about 1 teaspoon per 2 cups of water) outperformed both plain water and bleach at removing surface residues. It requires a 12–15 minute soak, and can’t touch residues that have penetrated beneath the skin — but it’s a useful tool if apples are a daily habit.

Frozen organic is a good thing. Frozen organic strawberries, blueberries, and spinach are nutritionally comparable to fresh and quite a bit cheaper.

The Half Sandwich Generation:

I’m child-free with aging parents

When people ask me if I have children, I’m tempted to respond, “Do two adult parents count?”

It’s not entirely a joke. For many of us midlife women who are child-free, whether by choice or by circumstance, caregiving hasn’t disappeared. It has simply shifted directions. Instead of raising children, many of us find ourselves supporting our aging parents. And unlike the well-documented “sandwich generation,” our experiences are quieter, less visible, and oftentimes, misunderstood.

And in the moments between being on hold with insurance companies (again) and navigating hospital bills, we might notice an even quieter thought: If I am the one taking care of everyone else, who will take care of me when I’m older?

The default caregiver

Meet Sarah*, a composite of many clients I’ve worked with over the years. She is in midlife and has always been the caregiver in her family, partly because she is the eldest daughter, but also because she has been labeled the most “competent.” Growing up, she helped raise her younger siblings while her parents worked multiple jobs. Somewhere along the way, her own needs became secondary.

Sarah had romantic relationships in the past, but when conversations turned to “starting a family,” the timing never quite worked. Either her partner was not ready, or she found herself on the fence, already worn down from caring for her siblings. Now she finds herself single and living alone. She works a stable job that pays reasonably well, but it offers little flexibility and comes with high healthcare costs. She knows she cannot easily step away from it.

Her parents are aging, and as expected, she has become the default caregiver. Her siblings live farther away and have children of their own, so much of the responsibility falls to her. She schedules doctor appointments, drives her parents to the grocery store, and reminds them when to take their medications. Their memory is starting to decline, and she worries how much longer they can live independently. At the same time, she knows she does not want to move in with them and wonders what kind of facility they could afford.

Financially, she is starting to feel the strain. After her father’s fall, she began dipping into her savings while waiting for disability support. She knows she should prioritize her own future, but that feels almost impossible when her parents need help now. Sometimes she goes on small shopping sprees just to release some of the pressure, but then finds herself struggling to pay off her credit cards.

Maybe you know someone like Sarah. Maybe you are Sarah.

You’re definitely not alone

In my work as a psychologist and certified financial therapist, I see this pattern repeatedly. Many of my clients do not have children, yet they carry significant caregiving responsibilities. They are coordinating medical care, helping with finances, and absorbing the emotional weight of their parents’ aging. At the same time, they are trying to build their own financial futures, often on a single income, without the buffer of a partner, and with the added pressure of what many refer to as the “single tax.”

This sits alongside another reality that is rarely discussed. Approximately one in six women in the United States reach their early 40s without having children and in recent Pew Research, a growing number are also unpartnered, meaning they are navigating both caregiving and financial planning on their own. Despite this, women without children are still often labeled, implicitly or explicitly, as “selfish,” “career-focused,” or lacking in care and responsibility.

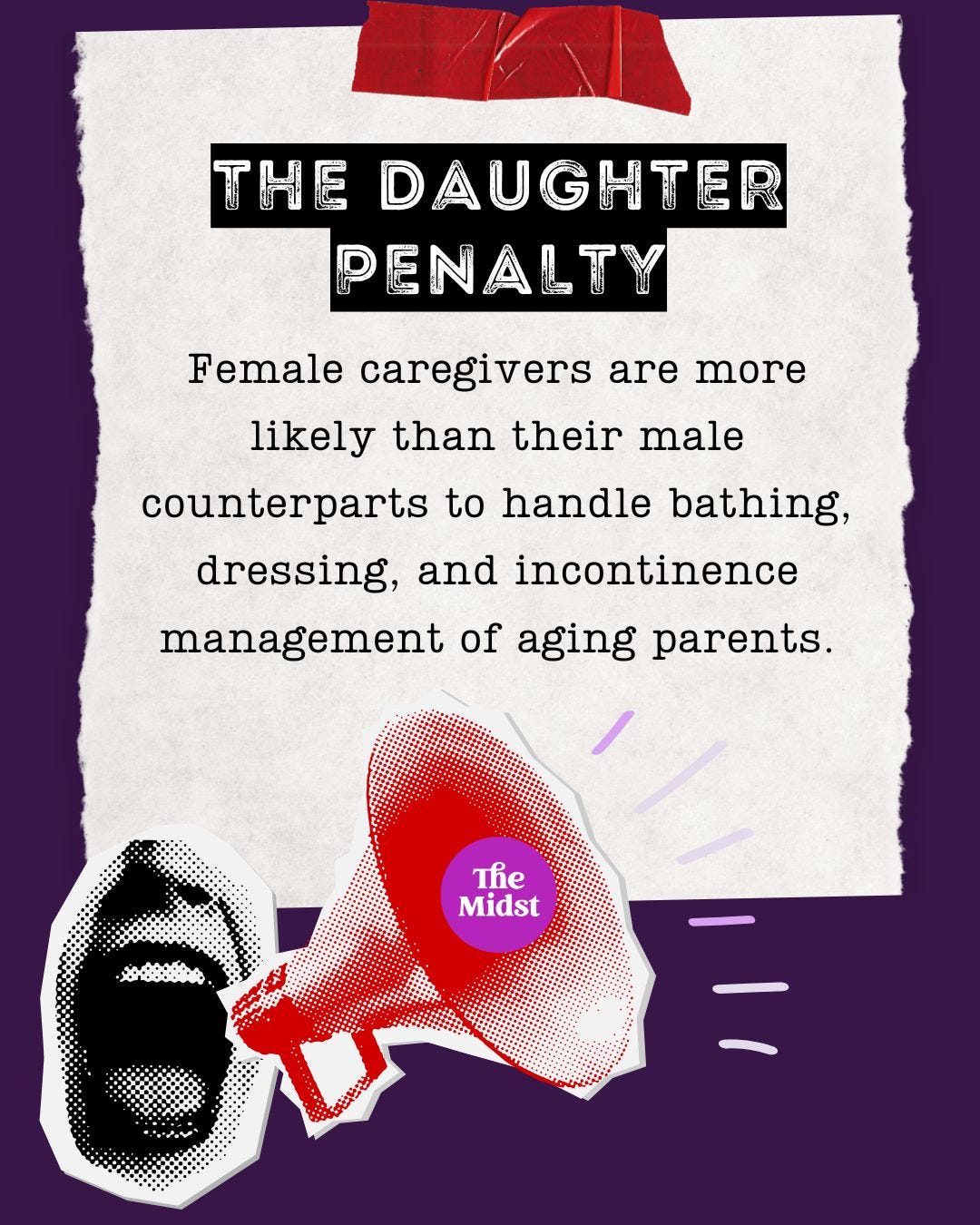

There is also what is now coined the “daughter penalty.” Women make up approximately 61%of caregivers in the United States and experience an estimated financial impact of around $7,200 per year in lost wages and out-of-pocket costs, according to a recent Forbes article. That number does not include missed promotions, reduced retirement savings, and the mental toll of consistently putting one’s own needs on hold. Unfortunately, much of this labor is still rarely questioned.

For women without children, caregiving can take on an additional meaning. There can be an unspoken message: at least you are taking care of your parents. For some, this brings a subtle and toxic sense of validation in a culture that otherwise judges their choices. Caregiving becomes not just a responsibility, but a twisted way to prove one’s worth or role in society.

My story

As I sit with clients like Sarah, I often find myself reflecting on my own upbringing as the eldest daughter of Vietnamese refugees. My parents were boat people who fled Vietnam in search of opportunity and worked in sweatshops, construction, and other labor-intensive jobs to make ends meet. Supporting my parents was never framed as a choice. It was a given. They would say, matter-of-factly, that they were investing in me so that one day I could help them. It was difficult to argue with people who had risked their lives for your future.

And yet, even as a child, there was a part of me that wanted to say, “But I didn’t ask you to get on that boat!” Even thinking that felt like a betrayal. Worse, it risked being seen as ungrateful. I often felt caught between two worlds, my collectivist family and a more individualistic, American context. I carried a quiet sense that I was somehow failing both. Not Vietnamese enough. Not America enough.

Over time, through my own therapy and professional training, I began to understand that it is possible to hold multiple truths. I can feel deep gratitude for my parents’ sacrifices and also feel anger and resentment at the implicit expectation that I would one day take care of them. Both are real. Both deserve space. Because of this, I have much more compassion for the younger grad- school version of me, the one horrified at the growing student loan balances while quietly shaming herself, wondering how she was supposed to support her parents when she could barely take care of herself.

Now I find myself thinking not only about how to support my parents, but also about my own future. How do I take care of myself in a way that preserves my mobility and independence? What kind of support system and community am I building now? And how do I make decisions while holding all of the roles I carry?

It is not an easy process. But it is one I must be willing to have with myself if I encourage my clients to do the same.

Practical starting points

Many of the thoughtful women who seek financial therapy with me express a desire for freedom, stability, and long-term security. At the same time, their financial decisions, particularly around caregiving, may conflict with those values. This is not because they are “bad with money” or lack discipline. It is the result of bigger competing forces, including cultural expectations, emotional bonds, and long-held beliefs about what it means to be a “good” daughter.

While every caregiving situation is different, here are a few questions that can start what is often a difficult set of conversations. Death and decline are not easy to talk about, but avoiding them usually makes things harder later.

Start by determining what is actually sustainable. Supporting a parent should not require sacrificing your own long-term financial stability. Providing care with dignity does not mean doing everything or doing it perfectly.

Have conversations early so that decisions are not made in crisis. This includes talking through finances, expectations, and preferences, and understanding what resources are already in place such as Social Security, retirement accounts, and other assets.

Put legal structures in place. Power of attorney, healthcare directives, and other documentation can prevent confusion, reduce family conflict, and make it easier to act when decisions need to be made quickly.

Assess available support. Even if it feels like the responsibility falls on you, it is worth taking a step back to look at the full picture. This might include extended family and community resources. Organizations like the National Alliance for Caregiving and AARP offer practical guides, planning tools, and education around navigating caregiving.

It is also important to recognize the signs of caregiver burnout. Chronic fatigue, irritability, resentment, and emotional numbness are not personal failures. They are signals that something needs to shift.

Finally, notice your internal responses. Before making financial or caregiving decisions, pause and ask what emotions are present and how they may be influencing your choices. Guilt, fear, and obligation can be powerful drivers.

Expanding the definition of care

Caregiving is oftentimes framed as something directed outward. What we give to others. However, sustainable caregiving requires expanding that definition to include ourselves.

This includes protecting our financial future, setting boundaries, and allowing space for our needs, relationships, and goals.

For those without children, this becomes especially important. Without the assumption of reciprocal care later in life (though, maybe that’s another assumption to be challenged?), intentional planning and self-investment are essential. More and more, I see women beginning to approach this differently: planning to age in place, building community with friends (a la Golden Girls), and creating alternative support systems.

So the question I keep coming back to, with myself and with my clients, is this: What would it look like to care for others without abandoning ourselves?

This story was first published here on the-midst.com.

*Names have been changed to protect identity.

Dr. Huong Diep, PsyD, ABPP, CFT, is a board-certified psychologist and Certified Financial Therapist whose work sits at the intersection of money, mental health, and identity. She works with individuals navigating caregiving, cultural expectations, and complex life transitions, helping them make decisions that honor both responsibility and self. Learn more at drhdiep.com and connect with her on Linkedin.

as the only daughter who is also unmarried, I really related to this